A Founder's Guide to Founders' Agreement Essentials in Australia

What a founders' agreement actually is

A founders' agreement is the document that answers all the awkward questions you're hoping you won't ever need answers to. Who owns what? Who decides what? What if someone wants to leave, or wants someone else to leave? What happens to the IP one of you built before incorporation?

It's not technically required by Australian law; you can start a Pty Ltd without one, but operating without one is a genuinely bad idea. Most startup disputes that end up in expensive litigation trace back to assumptions that were never written down, usually from a stage when everyone was still friends, and nothing seemed like it could go wrong.

How it fits with your other documents

Running a Pty Ltd in Australia, you'll typically end up with three interlocking governance documents. The Company Constitution sets out the rules for how the company itself operates; it replaces or modifies the "replaceable rules" in the Corporations Act 2001. The Shareholders Agreement governs the relationship between shareholders and the company, covering matters such as share transfers, drag-along/tag-along rights, and investor protections. The Founders Agreement sits alongside these and covers the specific founder-to-founder relationship, roles, commitments, vesting, and IP.

These documents need to be consistent with each other. If your founders' agreement says one thing and your constitution says another, you've got a problem that will surface at the worst possible time. A good startup lawyer drafts them as a package.

For very early-stage teams, a founders' agreement can be signed before incorporation as a kind of "handshake in writing." It becomes binding between the founders even before the company formally exists, and the substantive terms are then rolled into the proper governance documents once the company is incorporated.

The essential elements

1. Parties, the company, and the business

Name all the founders, identify the company (or the intended company if pre-incorporation), and describe the business concept clearly enough that you can later say "this project" and know exactly what you mean. This matters especially for IP assignment — if the business pivots later, you want to know which IP transferred.

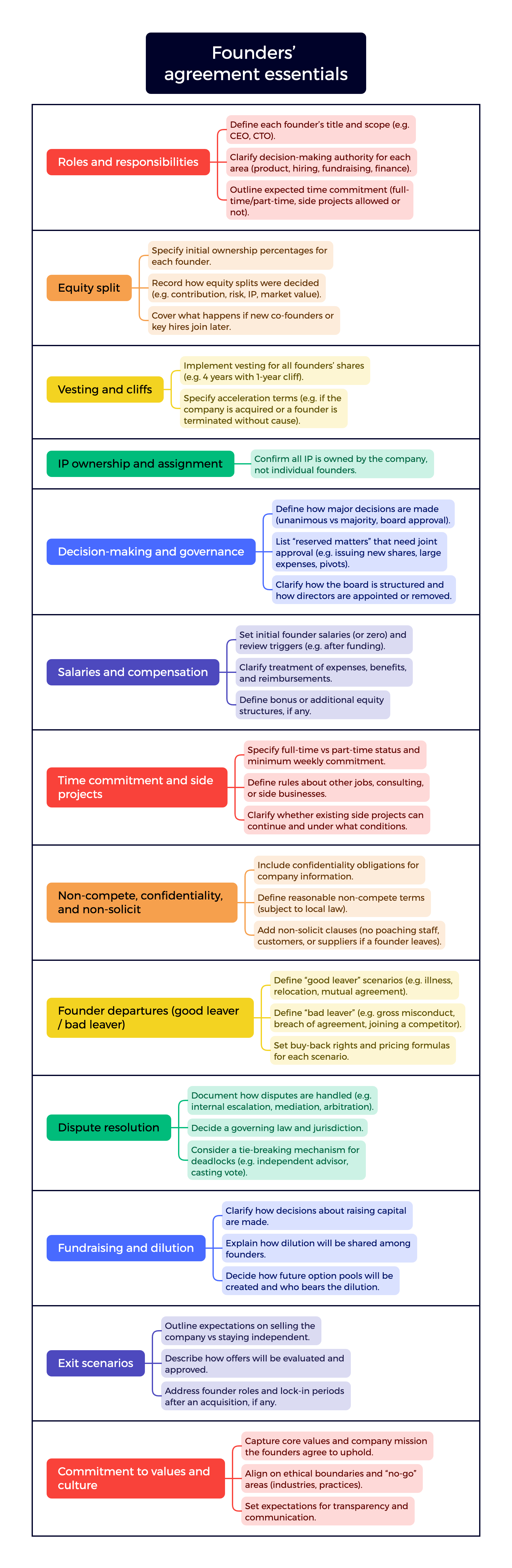

2. Equity split and capital contributions

The headline item. Who owns what percentage, and what did they contribute to earn it?

Equal 50/50 splits feel fair at the start, but often aren't. Different founders bring different things: capital, IP, full-time commitment, a network, a track record, and most experienced investors prefer to see an intentional split that reflects real contributions rather than a reflexive even division.

Capital contributions need to be documented precisely: who paid how much, for what shares, on what date. If anyone is contributing assets rather than cash, IP, equipment, or pre-existing code, document the valuation and treat it as a share-for-asset exchange with proper paperwork. "Sweat equity" is fine, but still needs to be documented as shares issued for services, and with care, because this can trigger tax consequences under the ESS rules discussed in the vesting guide.

Also, cover what happens when the company needs more money. Will founders top up pro rata? Will you only raise externally? Pre-emptive rights on new share issues belong here (or in the shareholders' agreement).

3. Roles and responsibilities

Assign titles (CEO, CTO, COO, etc.) and describe each founder's functional area. This prevents two people from thinking they're in charge of sales, or nobody from thinking they're in charge of finance. It also makes later hiring decisions cleaner.

4. Time commitment and exclusivity

Is each founder full-time? If not, how many hours per week? Are they allowed to keep a day job, advisory gigs, or a consulting practice on the side? For how long?

5. Salary and remuneration

Most early founders take little or no salary. But document the plan: no salary until Series A? Minimum living wage after first revenue? Equal salaries or differentiated? Also, address expense reimbursements. Trivial in theory, surprisingly contentious in practice.

6. Decision-making and governance

Separate day-to-day decisions from major decisions. Day-to-day stuff can usually be delegated to the CEO or made by majority vote. Major decisions, often called "reserved matters", should require unanimous consent from the founders or a defined supermajority. Typical reserved matters include issuing new shares or changing the cap table, raising capital or taking on significant debt, approving annual budgets, hiring or firing senior staff (including founders), signing material contracts above a dollar threshold, amending the constitution or shareholders' agreement, selling the company or material assets, and changing the company's core business.

Under the Corporations Act, directors owe duties to the company (not to individual shareholders or founders), and those duties can't be contracted out of. Your founders' agreement shapes how directors choose to act but doesn't override their statutory duties.

7. Vesting

Covered in detail in the previous guide. The short version: every founder should have a reverse vesting schedule (usually 4 years with a 12-month cliff), with clear good-leaver and bad-leaver rules and at least double-trigger acceleration on change of control. This either sits inside the founders' agreement directly or in a separate Share Vesting Agreement that the founders' agreement cross-references.

8. IP assignment — the single most important clause

This is the one that sinks startups at due diligence, so pay attention.

Australian law does not automatically assign IP created by founders to the company, even if they created it for the company. Without an explicit written assignment, the founder personally owns what they created, and the company has only an implied licence at best. Solid IP provisions should transfer to the company every piece of IP each founder has created in connection with the business — code, designs, inventions, trade secrets — explicitly covering pre-incorporation work, work done during the startup phase, and anything created throughout each founder's tenure.

When an investor runs due diligence on your Series A, their lawyers will go through every founder's contribution history with a torch and demand a clean chain of assignment. If you haven't done it properly, you'll be scrambling to get ex-founders to sign retrospective assignments — often with leverage they didn't have before.

Australian best practice means an explicit present assignment of all IP created by founders relating to the business (including pre-incorporation work), a future assignment of anything created during their involvement with the company, a moral rights consent (Australia has separate "moral rights" under the Copyright Act that survive assignment and must be expressly consented to), and specific coverage for any identified pre-existing IP — code, designs, documents, research, prototypes.

This applies to everything: the domain name registered on a personal account, the Figma file on a personal Dropbox, the GitHub repo under someone's personal handle. All of it needs to be owned by the company.

9. Confidentiality

Each founder agrees not to disclose or misuse confidential information during and after their involvement. Standard stuff, but important — and typically drafted so that genuinely confidential material stays protected indefinitely, not just for a defined period.

10. Non-compete and non-solicitation (restraints of trade)

Here's where Australian law diverges noticeably from the US.

Australian courts are genuinely hostile to broad non-compete clauses. They'll enforce restraints only to the extent they protect a legitimate business interest — confidential information, customer connections, goodwill — and are reasonable in scope, geography, and duration. Typical employment restraints run from about three months to two years, and any restraint should only protect the legitimate interests of the business. Common drafting uses a "cascading" clause (e.g. "12 months, or if that is unenforceable, 9 months, or if that is unenforceable, 6 months…") so a court can strike down the broadest version without invalidating the whole clause.

Non-solicitation clauses (don't poach our staff, don't poach our customers) are generally easier to enforce than outright non-competes. Worth having both.

Also worth noting: the federal government has flagged reforms to restrict or ban non-compete clauses for lower-income workers, and this area is shifting. Drafting should be checked against the current law when you sign, and reviewed again before any founder departure.

11. Conflicts of interest

Each founder must disclose any external business interests that could conflict with the company. This protects against a founder running a side venture that competes for their time, customers, or ideas, and gives the other founders a clean slate to raise issues if they arise.

12. Leaver provisions (for vested shares)

Vesting rules deal with unvested shares, but the founders' agreement (or shareholders' agreement) should also address what happens to vested shares when a founder leaves. Common structures include a right of first refusal for the company or the remaining founders over any sale, a prohibition on selling to a competitor, and, in bad-leaver scenarios, a compulsory buyback of vested shares at the lower of cost and market value.

13. Dispute resolution and deadlock

For small founder teams — especially 50/50 — deadlock is a real risk. Two equal shareholders who can't agree will freeze the company.

Build in an escalation ladder: direct discussion between founders, then mediation, then binding arbitration. In rarer cases, founders use a "Russian roulette" or "Texas shootout" buyout mechanism in which one founder names a price, and the other either buys at that price or sells at it. Mediation clauses keep disputes cheaper and more private than litigation, and most Australian commercial disputes start there anyway.

Always include a governing law and jurisdiction clause specifying Australian law and the state whose courts will have jurisdiction — usually the state where the company is registered or has its principal place of business.

14. Amendment mechanics

Amendment mechanics (usually requiring the written consent of all founders), execution in counterparts, entire-agreement clause, severability, and notices. These look like boilerplate, but they determine whether the agreement actually holds up when tested.